EBW is exploring our incredible history not just as a nation, but through the lens of our financial lives. The same qualities that help build lasting financial security - careful planning, strong foundations, and thinking beyond the present moment - reflect the mindset that helped shape our nation's beginning. We started in June by exploring the innovation it took to build a nation from scratch. We met the men who put their fortunes on the line for a new nation, Benjamin Franklin, Alexander Hamilton, Robert Morris, and Haym Salomon, and explored the financial philosophy that guided them.

This month, we examine how our young country's foundation grew. From the steam of the Industrial Age to the prosperity of the Post-War Boom, America didn't just survive….it scaled. And in doing so, innovators created something remarkable: tools that enable ordinary Americans to build extraordinary financial futures. We hope you enjoy the series.

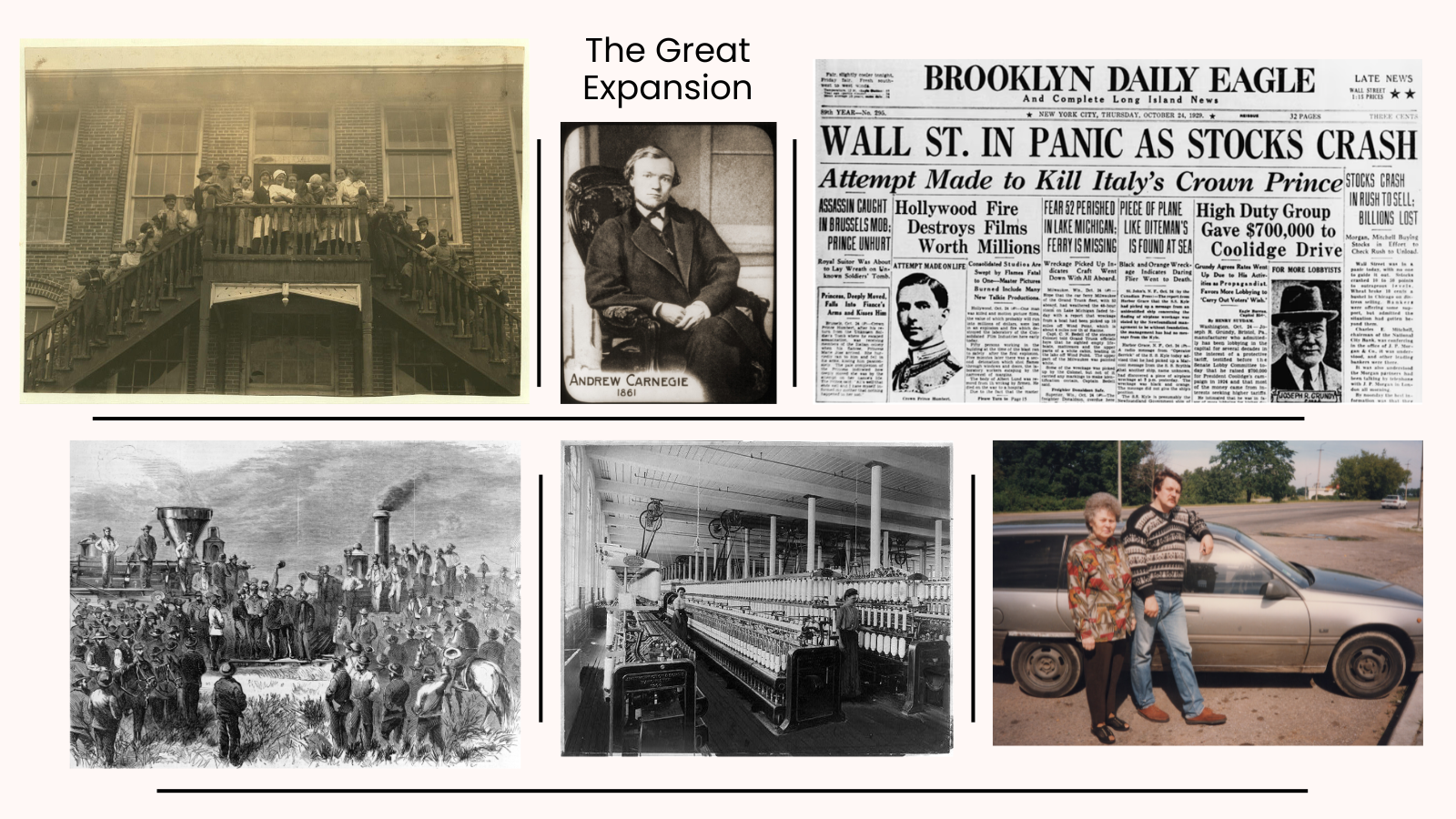

Lessons from the Industrial Age & Post-War Boom (1860s–1970s)

The country that fought for its financial life in the 1770s was, by the late 1800s, building railroads across a continent. Factories hummed. Cities swelled. And for the first time in history, wealth wasn't just for the wealthy. The great American middle class was born, not by accident, but by systems. Markets, pensions, compound interest, and eventually Social Security gave ordinary Americans access to tools that would change what a financial life could look like.

No figure captures this era better than Andrew Carnegie. A Scottish immigrant who arrived in America with nothing, Carnegie became one of the wealthiest men in history, though not without controversy.¹ This was the age of the so-called "robber barons," and Carnegie was among them. His steel empire was built on the backs of workers who endured brutal hours, dangerous conditions, and wages that barely sustained a family. The rise of labor unions during this era was a direct response to those very conditions, and their fight for fair pay and safe workplaces shaped the American workforce we know today.

Yet Carnegie's financial philosophy remains instructive. In his 1889 essay The Gospel of Wealth, he argued that accumulating wealth entailed a deep personal responsibility, a philosophy still debated today.² And however complicated his legacy, the mechanics of how he built his fortune are worth examining: disciplined reinvestment, compounding returns, and thinking not in days but in decades.³

Building the Foundation

Before the Industrial Age, building wealth was largely a matter of birthright and privilege. The railroad boom, the GI Bill of 1944, and the post-World War II economic expansion created new pathways to prosperity for many Americans. By 1951, the GI Bill had enabled more than eight million veterans to earn college degrees or receive on-the-job training, and helped millions more buy their first homes through low-interest loans.⁴ In a single generation, a new class of American wealth emerged, not through inheritance, but through access.

Yet that access was far from universal. Despite the GI Bill making no formal distinction by race, Black veterans across the country, and particularly in the South, were systematically denied its benefits. Local VA offices, segregated universities, and discriminatory lending practices shut out many of the men who had fought and sacrificed alongside their white counterparts.⁵ Their story is a reminder that economic progress has not always moved forward equally for all Americans.

Access to sound financial planning has always been the great equalizer. The tools of this era, including savings, investment, homeownership, and education, remain powerful and available to you today.

The Birth of Retirement

Before the twentieth century, retirement as a life stage essentially did not exist. Most Americans worked until their bodies gave out, and then depended on family or charity. There was no plan because there was no concept of one.

That changed in 1935, when President Franklin Roosevelt signed the Social Security Act into law.⁶ Born out of the devastation of the Great Depression, Social Security was the country's first formal acknowledgment that individuals couldn't be expected to fund old age entirely on their own. The person most responsible for making it a reality was Frances Perkins, FDR's Secretary of Labor, the first woman ever to serve in a U.S. Cabinet position.⁷ She spent years fighting to build the framework that millions of Americans still rely on today.⁸ It was a hard-won victory. The legislation faced fierce opposition from business interests and conservative lawmakers who argued the government had no place in the retirement of private citizens.

Eventually, the corporate world followed. In the decades after World War II, defined-benefit pensions became standard in American industry. For the first time, a factory worker, a teacher, or a postal employee could look forward to a guaranteed monthly income in retirement. The very concept of a "retirement plan" entered the American vocabulary. But that security was never as universal as it appeared. Not all industries offered pensions, and millions of workers, particularly those in low-wage jobs, domestic work, or agriculture, were left out entirely.

What worked for one generation looked very different for the next. By the 1980s, the defined-benefit pension was giving way to the 401(k), shifting the responsibility for retirement savings from employers to employees. Today, pensions are largely a relic of the past outside of government and some union jobs. The 401(k) is now the primary retirement savings vehicle for most working Americans, yet studies consistently show that nearly half of Americans have little to nothing saved for retirement. The decisions that were once made for you, how much to save, how to invest, when to draw down, are now entirely yours to make. That is both a freedom and a risk, which is precisely why having a thoughtful financial plan is not optional. It is essential.

The Power of Time: Investing and Compound Interest

If retirement gave Americans a destination, the markets gave them an engine to achieve it. Though not without some brutal lessons along the way.

The stock market boom of the 1920s introduced ordinary Americans to investing at scale for the first time. Fueled by speculation, easy credit, and unchecked optimism, it was also deeply unstable. The crash of 1929 didn't just wipe out portfolios. It wiped out life savings, shuttered banks, and pushed millions of families into poverty overnight. For many ordinary Americans who had just discovered the markets, it would be a generation before they trusted them again.⁹ The Securities and Exchange Commission was created in 1934 to restore confidence and bring order to markets,¹⁰ but rebuilding public trust took decades. Two decades later, Benjamin Graham's The Intelligent Investor re-engaged a wary public with the markets, laying the intellectual foundation for everything modern investing would become.¹¹ His central argument was a direct response to the speculative fever that caused the crash: the patient, disciplined investor will always outlast the speculator.

Warren Buffett, Graham's most famous student, later put it plainly: the stock market is a device for transferring money from the impatient to the patient.¹²

Compound interest is often described as the quiet engine of generational wealth, and the math bears that out. But it only works if you stay in the game long enough for time to do its work. The investors who panicked in 1929 and again during every subsequent downturn locked in their losses. The investors who held a diversified plan and stayed the course came out the other side. That pattern has repeated itself throughout every market cycle since.

The lesson tracks directly into your financial life today. Diversification, long-term thinking, and consistency aren't strategies invented by modern financial advisors. They were forged in the wreckage of the 1929 crash, tested through the downturns of the following decades, and proven over generations to be the most reliable path forward. The risk isn't the market. The risk is making emotional decisions when the market gets hard.

A Lesson in History

America's great expansion didn't happen by luck, and it wasn't without cost. Systems were built on the labor of workers who often didn't share in the wealth they created. Institutions were forged through crisis, failure, and hard political fights. And ordinary Americans learned, sometimes the hard way, that building a financial future requires more than optimism. It requires a plan.

The same truth holds today. The tools exist. Social Security, diversified markets, tax-advantaged retirement accounts, and the compounding power of time are all still working. But tools only work if you use them deliberately and consistently. Whether you are 25 and making your first investment, 50 and maximizing your retirement contributions, or 65 and thinking carefully about how to make your savings last, the window to act is always now, not later.

The history of this era is full of people who waited too long, trusted too blindly, or never had access to the right guidance. Your advisor is there to make sure that it is not your story.

Next month, we close our series with The Legacy Chapter: what we leave behind, and how intentional planning shapes the financial lives of those who come after us.

If you live in Fairfax County, learn more about 250th events by visiting America’s 250th. Live in Loudoun County, visit Loudoun Virginia 250. In Virginia, visit America Made In Virginia. In DC visit dc250.us. To find more information of 250th activities in your community, visit America 250 State and Territory Commissions website.

Footnotes

¹ Carnegie biography and the robber baron era: Biography.com, "Andrew Carnegie" — biography.com; History.com, "Robber Barons" — history.com; PBS American Experience, "The Homestead Strike" — pbs.org; U.S. Department of Labor, "The History of Labor Unions" — dol.gov

² Carnegie, Andrew. The Gospel of Wealth. 1889. Available via the Carnegie Corporation of New York: carnegie.org

³ Carnegie biography and business history: National Park Service, "Andrew Carnegie" — nps.gov; Carnegie Mellon University biography — cmu.edu

⁴ U.S. Department of Veterans Affairs, "History and Timeline of the GI Bill" — benefits.va.gov; National WWII Museum, "The GI Bill" — nationalww2museum.org. Note: verify enrollment figures against the VA or National WWII Museum before publication.

⁵ National Museum of African American History and Culture, Smithsonian Institution, "The Gift of the GI Bill" — nmaahc.si.edu

⁶ Social Security Administration, "Historical Background and Development of Social Security" — ssa.gov/history

⁷ U.S. Senate Historical Office, "Women in the Senate" — senate.gov; U.S. Department of Labor, "Frances Perkins Biography" — dol.gov

⁸ Frances Perkins Center — francesperkinscenter.org

⁹ History.com, "Stock Market Crash of 1929" — history.com; Federal Reserve History, "Stock Market Crash of 1929" — federalreservehistory.org; FDIC, "A Brief History of Deposit Insurance in the United States" — fdic.gov; Library of Congress, "The Great Depression and the New Deal" — loc.gov

¹⁰ U.S. Securities and Exchange Commission, "The Investor's Advocate: How the SEC Protects Investors" — sec.gov/about/history

¹¹ Graham, Benjamin. The Intelligent Investor. Harper & Brothers, 1949. Revised edition with commentary by Jason Zweig, HarperCollins, 2003.

¹² This quote is widely attributed to Warren Buffett but does not have a single verified original source. Recommend attributing as "widely attributed to Warren Buffett" in the text, or sourcing directly from Berkshire Hathaway shareholder letters — berkshirehathaway.com