FAQ's

What is a financial advisor?

A financial advisor helps individuals and families make informed decisions about their money so they can achieve their long-term goals. At EBW, this means creating personalized, growth-oriented financial plans based on your values, current situation, and future priorities, and providing ongoing guidance as your life evolves.

What is a CERTIFIED FINANCIAL PLANNER® (CFP®)?

A CERTFIFIED FINANCIAL PLANNER® (CFP®) professional is a trained and vetted financial advisor who meets rigorous education, exam, experience, and ethical standards set by the CFP Board to provide holistic, fiduciary planning.

Are you a fiduciary, and what does it mean to be a fiduciary?

Yes, we are fiduciary financial advisors.

A fiduciary is an individual or organization that is legally and ethically required to act in another person’s best interests. In a financial planning relationship, this means the advisor must put the client’s interests ahead of their own at all times when providing advice or making recommendations.

Being a fiduciary creates a relationship of trust. Clients rely on fiduciaries for expert guidance, often when making complex or high-stakes financial decisions, and fiduciaries are expected to act with loyalty, care, and transparency in managing those responsibilities.

At EBW, we are held to the fiduciary standards set by both the Securities and Exchange Commission (SEC) and the CFP Board. As Certified Financial Planners®, we commit to acting as fiduciaries whenever we provide financial advice and financial planning. In practical terms, this means our recommendations are driven by what is in our clients’ best interests, not by commissions, sales incentives, quotas, or product-driven compensation.

It is important to note that not all financial advisors are required to meet a fiduciary standard. We believe this distinction matters, and we view the fiduciary obligation as foundational to the trust our clients place in us.

What are your qualifications and experience?

When choosing a financial advisor, it is important to understand their education, professional credentials, and experience. These factors help ensure your advisor has the knowledge and background necessary to provide thoughtful, reliable guidance.

At EBW Financial Planning, we have been serving clients for more than 20 years, offering experienced guidance through an independent, fiduciary model that prioritizes our clients’ best interests. Our team includes professionals who hold respected industry designations such as Certified Financial Planner® (CFP®) and Accredited Investment Fiduciary® (AIF®), reflecting advanced education, rigorous standards, and ongoing professional development.

We are guided by a set of long-standing principles focused on elite standards of care, service, and communication. Our advisors take an approachable, transparent, and educational approach by working to understand your values and goals and delivering personalized financial plans that adapt as your life evolves. Our commitment is to provide clarity, confidence, and ongoing support at every stage of your financial journey.

As a financial advisor, what kinds of people do you commonly work with? Do you have a niche?

At EBW, we work with individuals and families from a wide range of backgrounds and life stages. Rather than focus on a single niche, our experiences span many situations we see most often in our day-to-day planning work, including:

- Federal, State, and County government employees

- Employees of government contractors, from small firms to large organizations

- Small business owners or self-employed professionals, such as realtors, consultants, and attorneys

- Individuals with employer stock benefits, including restricted stock units (RSUs), stock options, or private equity

- Families in a variety of circumstances, including widows and widowers, those navigating divorce, blended families, and families with special-needs considerations

This breadth of experience allows us to tailor financial plans to each client’s unique goals, responsibilities, and life stage.

What kind of services do you provide?

At EBW, we provide comprehensive financial planning, helping clients address nearly every area of life that involves financial decisions. Our approach is designed to bring clarity, coordination, and confidence across both short-term priorities and long-term goals.

Our services commonly include:

- Retirement planning – Helping you define when and how you want to retire and building a strategy to support that vision.

- Cash flow and budgeting – Ensuring day-to-day needs are met while supporting long-term goals through thoughtful income, expense, and debt management.

- Education planning – Evaluating options and planning for the cost of higher education based on your family’s priorities.

- Major goal planning – Supporting decisions such as purchasing a home, charitable giving, or leaving an inheritance.

- Investment management and guidance – Developing an investment strategy aligned with your goals, and providing ongoing management where appropriate, as well as guidance on employer-based plans such as 401(k)s or the Thrift Savings Plan (TSP).

- Employer benefits planning – Helping you understand and make informed decisions about the benefits available to you and your family.

- Insurance and risk planning – Identifying potential risks and evaluating strategies to help protect you and your family if the unexpected occurs.

Tax planning and estate planning are also critical components of a comprehensive financial plan. While we are not tax or estate attorneys, we incorporate these considerations into our planning process and coordinate closely with your existing professionals. When needed, we can also provide referrals to trusted tax or estate planning professionals to help ensure strategies are aligned and implemented effectively.

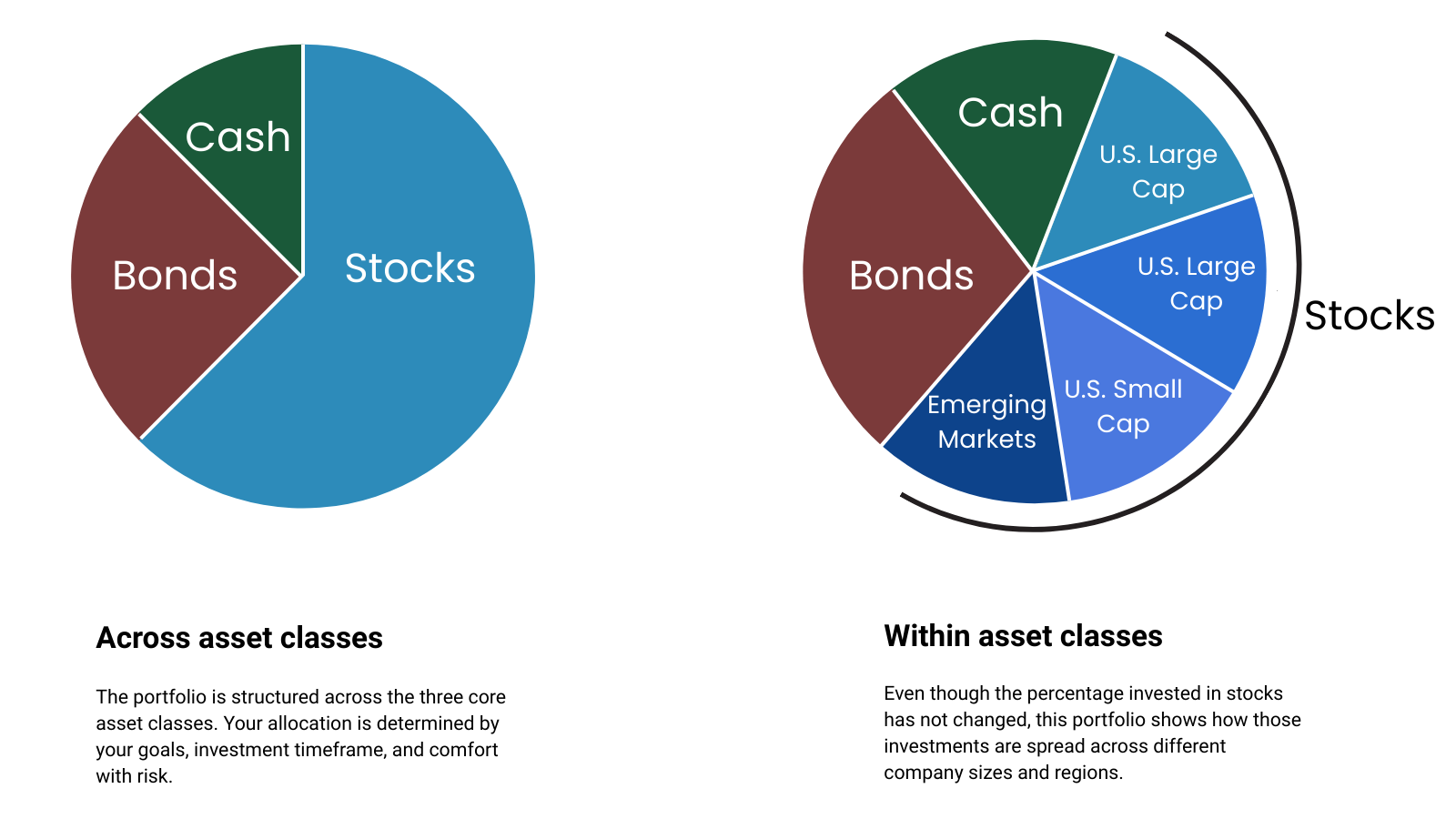

What is your investment approach?

Our investment approach is grounded in understanding you first. Before developing any strategy, we take time to understand your values, priorities, and financial goals, as well as your comfort with risk.

With that foundation in place, we design portfolios with a clear purpose, achieving their financial goals both long and short. Our portfolios seek total return utilizing both debt and equity instruments as well as alternative investments and cash. Our aim is not to create the highest rate of return, but to minimize the amount of risk associated with investing while achieving a realistic rate of return in order to achieve one’s financial goals. We utilize asset allocation strategies founded in Modern Portfolio Theory.1

How do you stay updated on market trends and changes?

The financial landscape is constantly evolving, and staying informed is a critical part of our responsibility to clients. At EBW, we continuously monitor market conditions, economic developments, and regulatory changes that may impact financial plans and investment strategies.

Our advisors pursue ongoing professional education, maintain required certifications, and regularly engage with industry research and planning resources. Just as important, we focus on applying new information thoughtfully by adapting strategies when appropriate while staying aligned with each client’s long-term goals and financial plan.

I'm not retired yet, should I have a financial advisor?

Yes. Our planning process is designed to provide meaningful value at every stage of life, not just in retirement.

Financial planning, much like investing, benefits from starting early. The earlier you put a plan in place, the more flexibility and opportunity you have over time. Working with a financial advisor before retirement allows you to make informed decisions around saving, investing, benefits, taxes, and major life goals long before they become urgent.

Whether retirement is decades away or just over the horizon, having a clear plan helps ensure the choices you make today support the future you want.

What can I expect when working with a financial advisor?

Every client’s situation is unique, and our goal is to provide advice that is tailored to your specific needs and goals. We follow a comprehensive financial planning process designed to provide clarity, structure, and ongoing support.

Our relationship begins by taking the time to understand your full financial picture and what matters most to you. From there, we analyze the relevant information, develop personalized recommendations, and work with you to put those strategies into action.

Financial planning is not a one-time event. As your life and financial circumstances change, your plan should evolve as well. Ongoing monitoring and regular review are essential parts of our process.

When working with a new client, this typically involves a series of initial meetings covering key areas of your financial life, including retirement and other long-term goals, investments, insurance and risk considerations, estate planning coordination, and other relevant topics.

Once the relationship is established, we continue to meet as needed to review progress, adjust strategies, and address new priorities. At a minimum, this usually includes an annual review, with additional meetings scheduled as life events or changes occur.

How and where can we meet?

Our office is located at 1919 Gallows Road in Tysons Corner, and we are always happy to meet in person when that is most convenient for you.

We also regularly meet with clients via Zoom or by phone, and work with individuals and families across the country. Whether in person or virtual, our goal is to make meetings accessible, comfortable, and effective tailored to your preferences.